Myths and reality: AI workforce dynamics across the Fortune 500

Widespread workforce impacts through the automation of work have been forecast for over a decade, kicked off by the groundbreaking estimation that “around 47% of total US employment could be automated over the next decade or two.”[1] Since then, more than 20 million payrolled jobs have been added in the US.[2]

- “Corporate America is convinced: Fewer employees means faster growth”

- “New technologies like generative artificial intelligence are allowing companies to do more with less”

- “Many companies are moving toward using more agentic AI, autonomous bots that can make decisions and complete tasks on behalf of humans.”[3]

Skepticism is healthy for two reasons

Firstly, markets reward corporate announcements of AI-driven workforce cuts. Take Block’s 25% share bounce when the fintech announced a 40% reduction in force. Respected business publications reported these cuts as “one of the clearest signs of the sweeping changes AI tools are having on employment,”[4] signaling “how the AI boom is translating from hype into workforce changes.”[5]

But comparing CEO Jack Dorsey’s claims with his company’s statutory annual report reveals an intriguing contrast. Dorsey referred directly to an AI-enabled productivity revolution, saying:

“Intelligence tools have changed what it means to build and run a company. A significantly smaller team, using the tools we’re building, can do more and do it better. I don’t think we’re early to this realization. I think most companies are late.”[6]

But close reading of Block’s 10-K report reveals a more circumspect outlook: a risk-laden talent-and-tech transition which may fail to deliver, as the following excerpt shows:

“We may not realize the expected cost savings, operating efficiencies, or other anticipated benefits of these initiatives within the anticipated timeframe, or at all. … Our ability to successfully operate with a reduced workforce is expected to depend in part on the effectiveness, reliability, and adoption of our proactive intelligence and AI tools … [which] … may not perform as expected … or may fail to enhance productivity and maintain operational efficiency.

“These actions could increase the risk of operational disruptions, service interruptions, control failures, or other significant events, particularly during transition periods, as responsibilities are reassigned and processes are adjusted.”[7]

The second reason for cautious skepticism stems from the dominance of heavily invested technology companies in media coverage. Capital spending by four “hyperscalers”—Amazon, Meta, Alphabet, and Microsoft—has more than doubled over the last two years from $140.1 billion to $357.3 billion and is set to continue on this exponential path.[8]

Commentary focused primarily on tech company going all-in on AI, which focuses only on layoffs without the wider context of hiring, and which detaches workforce size fro top-line performers risks creating a “reality-detached zeitgeist”.

Orgvue has analyzed 10-K annual reports filed by Fortune 500 companies since 2022[9] to reveal the reality of changing workforce dynamics, the relationship between workforce size and revenue performance, and the cost of organizational restructures.

Furthermore, every reference to AI has been dissected to reveal how AI is really showing up across America’s largest corporations. Our data-driven insight challenges prevailing narratives, providing a timely reality check with clear implications.

Myth versus reality

| Myth | Reality |

|---|---|

| #1 Organizations are slashing their workforces | The combined Fortune 500 workforce continues to incrementally increase Headcount growth by companies increasing their workforces added 580K employees, outstripping decreases made by companies reducing headcount (-543K employees). |

| #2 Technology companies are at the forefront of workforce reductions | The highest rate of workforce growth is seen across companies in the information technology sector Most companies (59%) reported headcount increases last year, adding 190K employees. |

| #3 Corporate restructures are being driven by AI adoption | AI or automation was referenced in less than 10% of reported restructures Reducing workforce costs and removing organizational complexity remain the predominant transformation triggers. Huge costs are incurred: $49.7 billion in employee severance alone. |

| #4 Companies are “doing more with less”; delivering revenue increases with a reduced workforce | Revenue growth continues to be fueled by the human workforce. Companies “doing more with less” were outnumbered and outperformed by peers investing in “human-fueled growth” 23% of companies did more with less in 2025, but a greater proportion (40%) increased their workforces to deliver top-line growth. Companies investing in human-fueled growth delivered revenue increases almost two times greater than those doing more with less. Doing more with less is not sustained over time: only 7% of companies pulled this off over two consecutive years; only 2% over three years. |

| #5 AI is being leveraged to deliver business benefits | Risk outweighs reward in company reporting of AI Almost all companies (94%) report AI as a potential risk factor, with individual companies reporting multiple sources of risk. 42% of companies report AI as a source of top-line value. But only 27% report AI in their internal operations referencing a specific use case or functional application. |

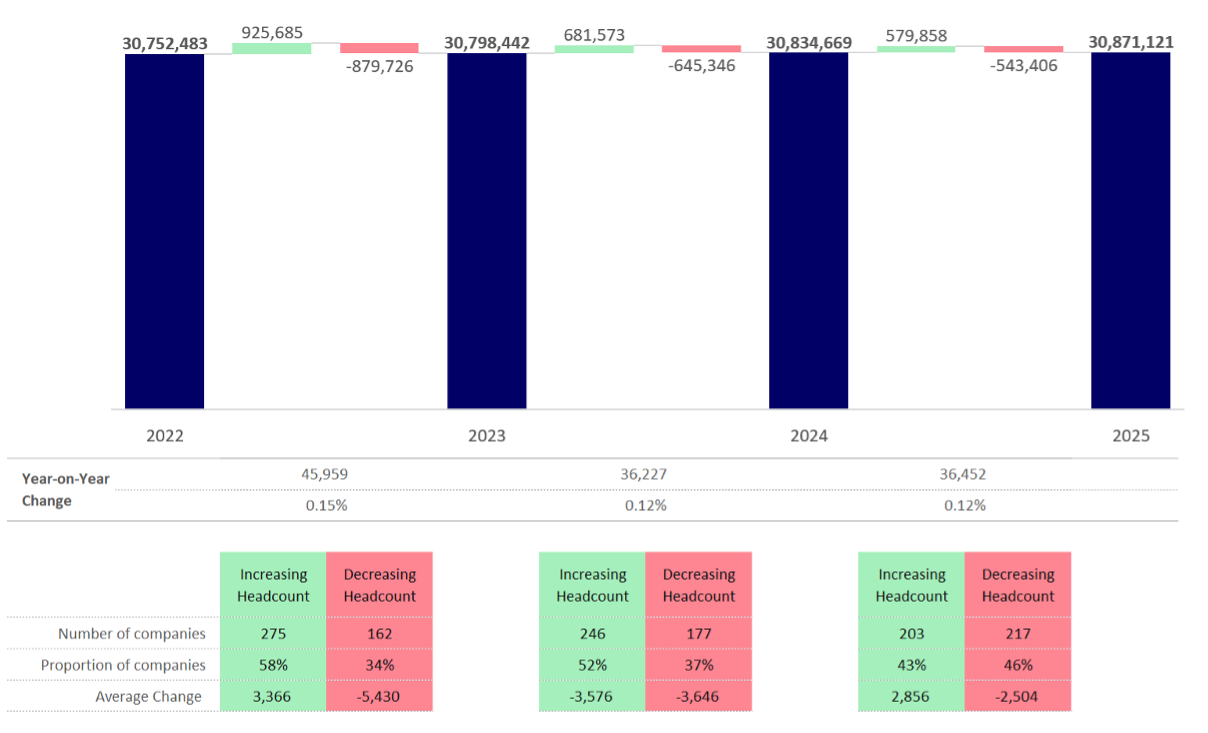

Myth 1: Organizations are slashing their workforces

Reality: The combined Fortune 500 workforce continues to incrementally increase.

- The proportion of companies reporting headcount decreases has risen for the last three years (34%, 37% and 46% in 2023, 2024 and 2025 respectively). Notably, in 2025 the proportion of companies reporting headcount decreases (46%) exceeded the proportion of companies reporting headcount increases (43%).

- Despite this trend, the combined Fortune 500 workforce increased as companies added more employees (+580K) than were cut by companies scaling back (-543K).

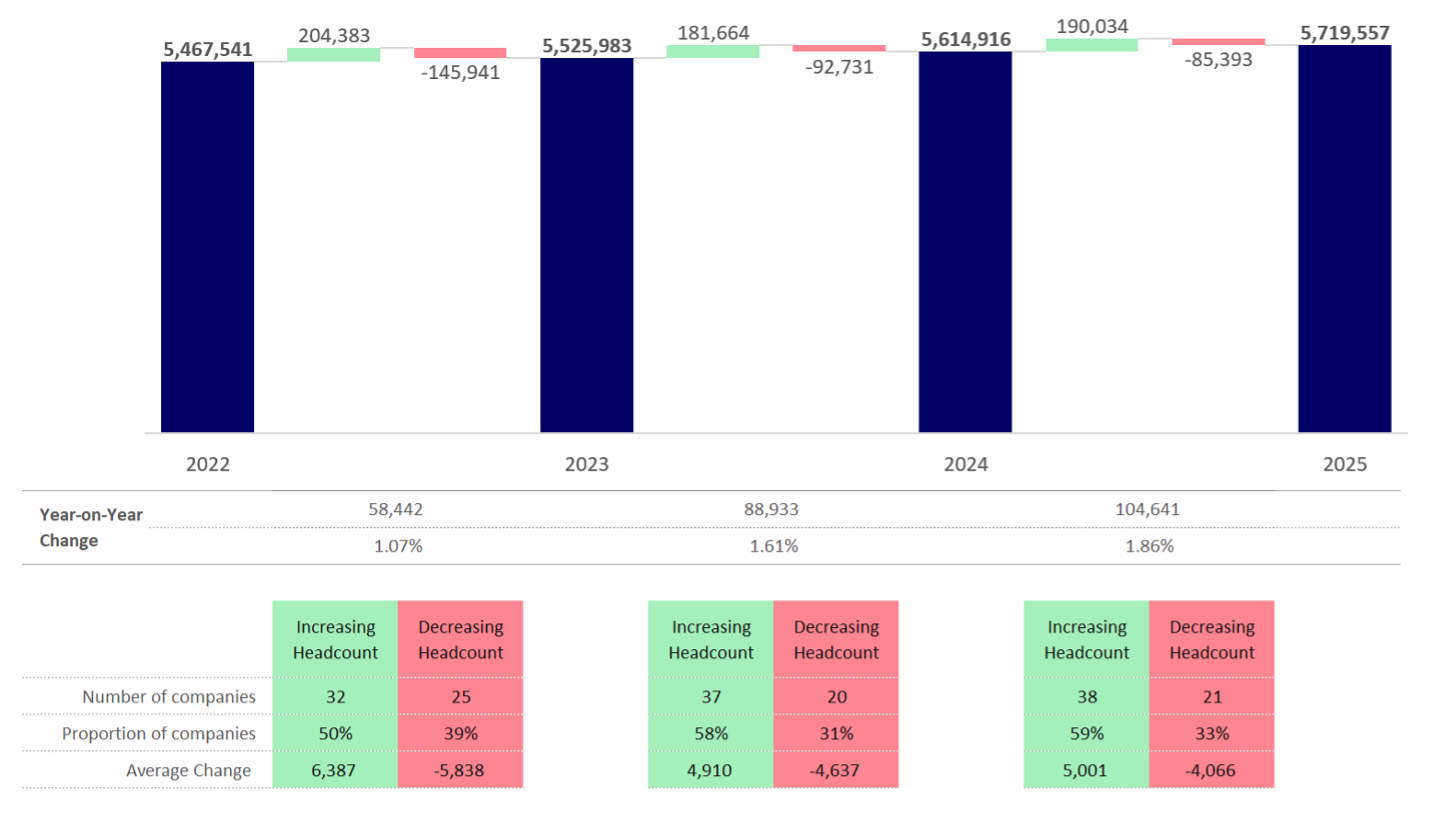

Myth 2: Technology companies are leading AI workforce reductions

Reality: The highest rate of workforce growth is seen across companies in the information technology sector.

- Most companies in the information technology sector (59%) increased their workforce last year, adding 190,034 employees.

- This headcount growth was offset by 33% reporting decreased headcount totaling 85,393 employees.

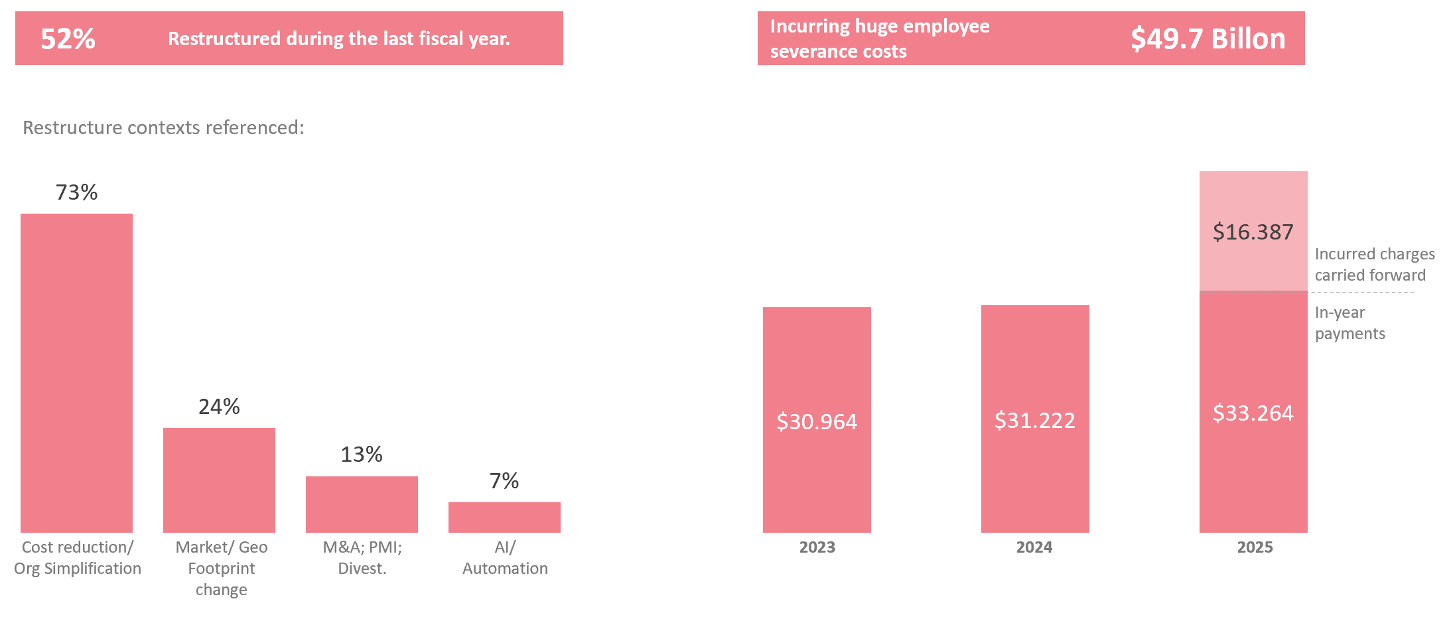

Myth 3: Corporate restructures are being driven by AI

Reality: AI and automation were referenced in less than 10% of reported restructures. Reducing workforce costs and removing organizational complexity are still the main triggers for transformation.

- 52% of companies reported organizational restructures last year.

- Almost three quarters of these restructures (73%) were driven by cost reduction or organizational simplification. A quarter (24%) referenced footprint changes relating to markets, geographies or specific locations. One-in-ten (13%) referenced post-merger integration or divestitures[10].

- Companies incur huge costs as they reduce and realign their workforces. Collectively, they recorded $49.7 billion in restructure-related employee severance charges last year.

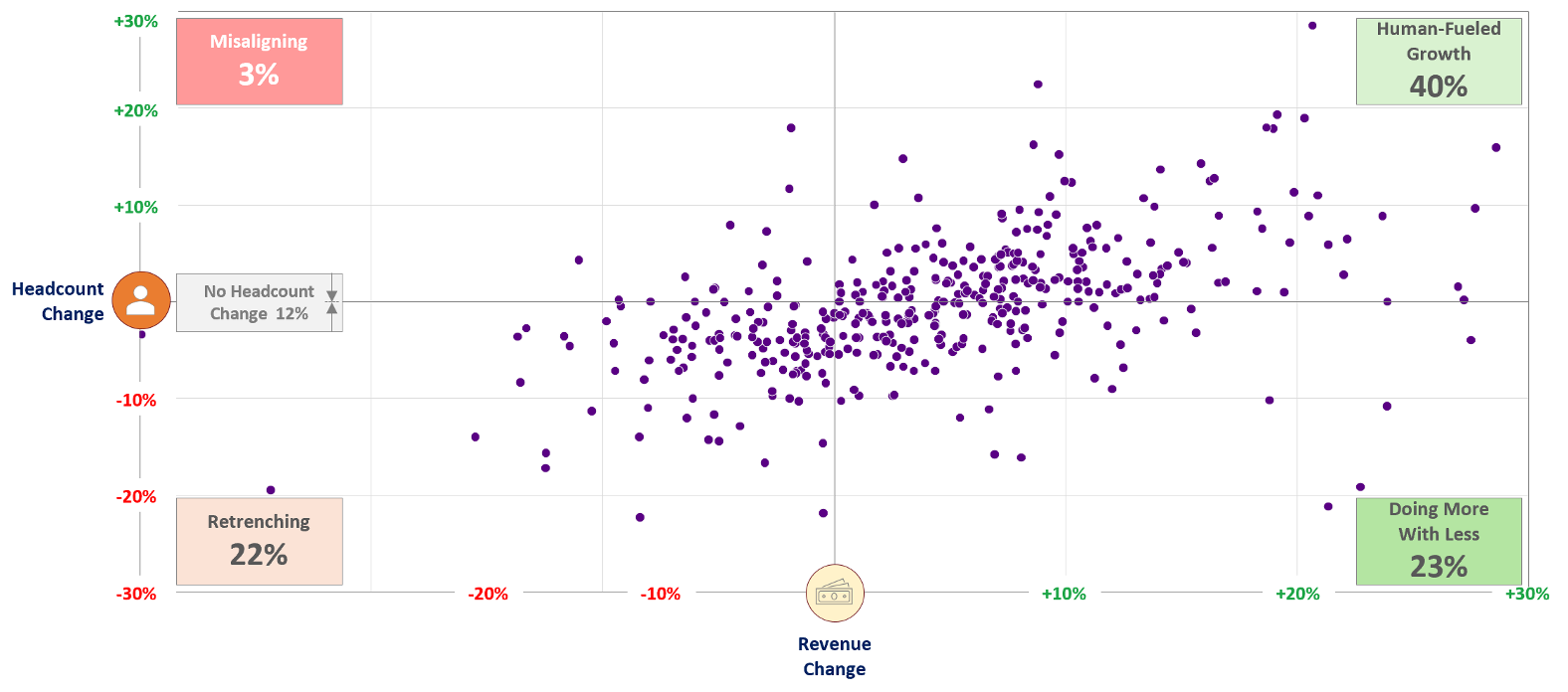

Myth 4: Companies are “doing more with less”, delivering revenue increases with a reduced workforce

Reality: Revenue growth continues to be fueled by the human workforce. Companies doing more with less were outnumbered and outperformed by peers investing in “human-fueled growth”.

- The proportion of companies doing more with less has increased year on year: 15%, 19% and 23% in 2023, 2024 and 2025 respectively.

- However, a greater proportion produced “human-fueled growth” by increasing their workforce to deliver revenue increases: 43%, 41% and 40% in 2023, 2024 and 2025 respectively.

- Doing more with less is not sustained over time: only 7% of companies pulled this off over two consecutive years and only 2% over three years.

- Companies investing in human-fueled growth delivered revenue increases two times greater than those doing more with less (12.4% compared to 6.8%).

Myth 5: AI is delivering business benefits

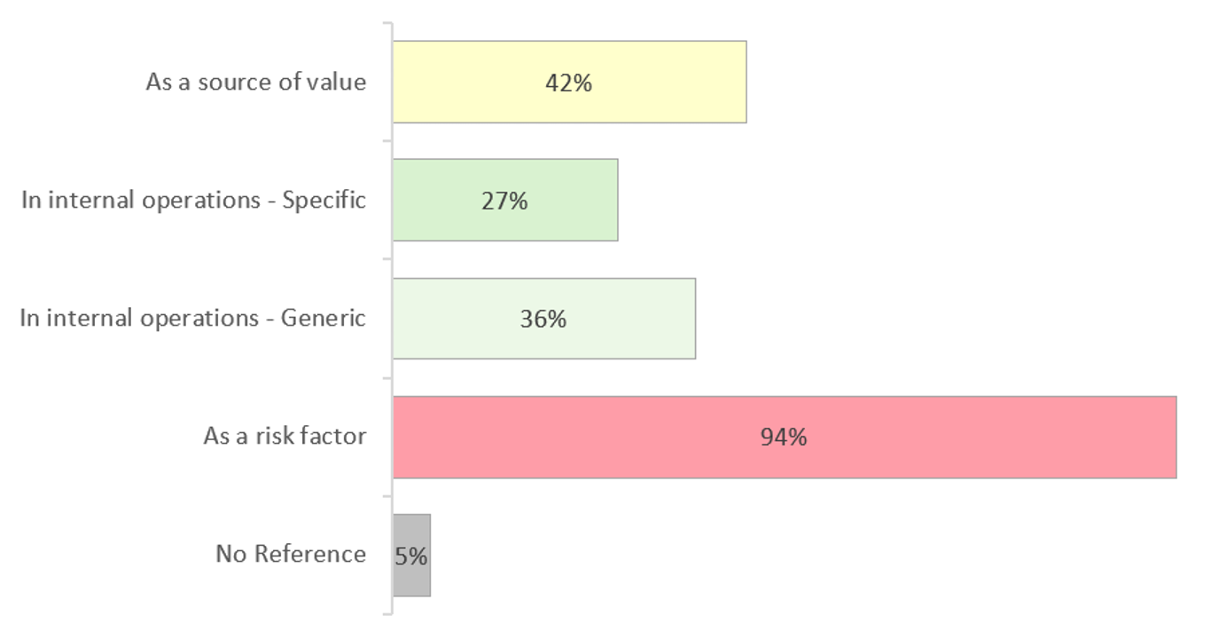

Reality: Risk outweighs reward in company reports.

- AI features prominently in 10-K statutory reports, with the number of references increasing 48% to more than 9,500.[11]

- Only 27% of Fortune 500 companies report AI being applied in their internal business operations, referencing a specific use case or functional application.

- A minority of companies (42%) reference AI as a source of top-line value.

- Almost every company (94%) reports AI as a potential source of business risk.

AI as a source of value

Less than half the Fortune 500 (42%) report AI as a source of value:

- Through AI-enabled products and services.

- By providing the components, infrastructure, energy, and finance required to sustain the AI value chain.

- By providing advisory services related to AI.

- Through the monetization of proprietary data and content.

AI in business operations

36% of companies report AI in internal business operations, with only generic statements or sentiment expressing future intentions. These are weak signals of AI application, typically found in the context of risk reporting. For example:

“Our business may be adversely affected if we cannot continue to successfully integrate artificial intelligence into our business processes.”

The most frequently referenced settings were customer contact and support; manufacturing and production; supply chain, logistics and inventory management; sales and marketing; risk management and fraud prevention (predominantly, but not exclusively, in financial services); and software engineering. Further examples are found across product development, people management, and business administration.

AI as a source of risk

The reporting of AI as a risk factor was near ubiquitous—reported by 94% of companies—with individual companies typically referencing multiple risk factors. These are summarized below:

- Market disruption and increased competition, including new entrants as barriers to entry are reduced.

- AI investments may not deliver returns, as customer adoption may not materialize and internal benefits may not be realized.

- Operational risk through AI producing outputs, which are flawed or difficult to explain (especially in financial modeling).

- Regulatory compliance and curtailment with an increasingly complex, burdensome, and costly regulatory environment to be navigated, which may prevent applications.

- Intellectual property loss and infringement.

- Energy availability and cost due to generation and distribution demands from data centers.

- Supply chain dependencies—the high dependency on a limited number of providers able to supply the infrastructure and components required for data center build out.

- AI talent scarcity and workforce transitions—risking the delivery of AI strategies or leading to workforce cost inflation.

- Stakeholder perceptions of AI potentially impacting corporate reputations and AI adoption.

- Heightened cybersecurity exposure and bad-actor threats becoming more sophisticated, difficult to protect against, and detect.

Implications for AI and workforce transformation

Our analysis challenges the prevailing narrative around AI workforce dynamics. We see four implications:

Don’t get caught in the hype

“Fear of missing out” is an understandable reaction to business coverage reporting a breakthrough year, with companies delivering faster growth with fewer employees. But “doing more with less” is out of reach for most companies, delivers inferior revenue growth and is not sustained over time. Beyond headline-grabbing corporate announcements, a complex, risk-laden, talent-and-tech transition is reported.

Fix the organizational infrastructure

AI isn’t a panacea for longstanding organizational weaknesses. It’s not going to fix a broken process. It’s not going to deliver double-digit growth in a structure with double-digit layers. Even the largest technology companies portrayed as going all-in on AI focus on the table stakes of organizational effectiveness: simplifying the processes and structures within which AI will operate.

Tracked-back to 2024, Amazon has been intentionally reducing organizational complexity: purging bureaucracy, flattening their organizations and reducing the proportion of managers. If AI is deployed in complex structures, where effort is duplicated, where accountabilities are unclear and governance is insufficient, organizational dysfunction exacerbate and costs will bloat.

Understand the work to plan the future workforce

It’s called a workforce for a reason. AI impacts work, automates existing work, and creates new responsibilities (managing the lifecycle of AI assets, overseeing outputs and holding accountability for outcomes).

With AI impacting most roles fractionally, a complex planning equation emerges involving automation potential, cost for compute relative to cost of employees, role redesign, and talent redeployment. Without a cost-based, process-led view of the current organizational reality and the ability to model how the workforce is impacted by changing work, transformational change will come with material unintended consequences, huge financial cost, and excessive human impact.

Manage ambiguity with intentional, incremental action

2026 is being called the year of the “mega-layoff”, how “instead of laying off people in more incremental—and less disruptive—waves, employers are using the potential financial upsides of severing swaths of their workforces at once.”[13] That may be a viable option for the high rollers who can drop a billion in severance without breaking stride, but reduction-in-force risks are material for most; “unintended consequences and costs, attrition beyond the intended reduction, the distraction of employees, reduced employee morale, [and] greater difficulty hiring new employees.”[14]

The factors underlying most of last year’s $50 billion employee severance bill—organizational complexity and workforce cost inefficiencies—didn’t emerge overnight; issues deteriorated until the transformation trigger needed to be pulled.

Incremental intentional action affords the most effective route to transformational outcomes. And being adept at adapting is the only way to navigate fast changing opportunities and risks presented by AI. Big bets are for the few; most will need to place their stakes deliberately and incrementally evaluating constantly changing odds.

Sources

[1] Frey, C. B. and Osborne, M. (2013) The Future of Employment. Oxford Martin School. University of Oxford.

[2] Orgvue analysis of US Bureau of Labor Statistics data.

[3] Wall Street Journal extracts.

[4] Financial Times. 26 February 2026. Block to cut workforce by ‘nearly half’ as it leans on AI tools.

[5] Reuters, 26 February 2026. Jack Dorsey’s Block to cut nearly half its workforce in AI overhaul, shares surge.

[6] Block Q4FY 2025 Shareholder Letter.

[7] Block, Inc 10-K filed 26 February 2026. Secondary emphasis.

[8] Alphabet has announced plans to double its investments from $90 billion to $180 billion in 2026, tied directly to their “AI Infrastructure”. Alphabet Shareholder Letter, “A note from Sundar, April 2026”.

[9] This year’s analysis is based on 475 companies, includingentrants to the list published June 2026. This base excludes companies that do not file a 10-K report (private companies and mutuals). Analysis is based on a consistent set of companies to enable comparisons over time, unaffected by changes to the composition of the Fortune 500. Companies merging with other Fortune 500 companies are excluded to avoid inflating headcount change values. 10-K reports are SEC-regulated, providing ‘a comprehensive overview of the company for the past year.’

[10] The total exceeds 100% because more than one restructure context may apply.

[11] Despite being ‘a comprehensive overview of the company for the past year’, it could be contended that relying on 10-K reports as a data source introduces reporting bias skewed towards risk. For completeness, and to overcome risk of bias, our analysis has extended to include – where available – reference to AI in companies’ Annual Report to Stockholders (ARS), Proxy Statements or Letters to Stockholders. These additional data sources were referenced for 341 companies. The volume of AI reporting shown above is based only on the regulated 10-K filings.

[12] Staying nimble and continuing to strengthen our organizations, Amazon News, October 28, 2025. Also, Update on our organization. Amazon News, January 28, 2026.

[13] Wall Street Journal, Has the Era of the Mega-Layoff Arrived? April 15 2026.

[14] Fortune 500 company 10-K filing.

Organizational design

Use Orgvue to restructure your organization.

Table of contents

- Skepticism is healthy for two reasons

- Myth versus reality

- Myth 1: Organizations are slashing their workforce s

- Myth 2: Technology companies are leading AI workforce reductions

- Myth 3: Corporate restructures are being driven by AI

- Myth 4: Companies are “doing more with less”, delivering revenue increases with a reduced workforce

- Myth 5: AI is delivering business benefits

- Implications for AI and workforce transformation

- Sources

Related posts

Ebook

Human first, machine enhanced: Deriving value from AI-driven workforce transformation

Ebook

Human first, machine enhanced: Deriving value from AI-driven workforce transformation

Article

Measuring the return of investment from AI deployments

Article

Measuring the return of investment from AI deployments